Chapter 11 Excise Duty

Excise Duty is an indirect tax charged on specific consumer goods such as tobacco, alcohol, fuel, and luxury products, often at production or import stage. In different countries, it may also be called Excise Tax or, informally, Sin Tax when the policy is intended to discourage consumption such as tobacco, alcohol, or gambling.

| English Name | Meaning | Notes |

|---|---|---|

| Excise Duty | Excise tax | Common official term |

| Excise Tax | Specific goods tax | Common in the United States |

| Sin Tax | Informal policy term | Often used for tobacco, alcohol, gambling, and similar goods |

Calculation Logic

Excise duty is often charged according to a product measurement basis. For alcohol, it may depend on alcohol content. For tobacco, it may depend on pieces or weight. The exact standard depends on local tax rules.

Unlike ordinary VAT, excise duty is often not simply sales amount multiplied by a percentage. It may be calculated by milliliter, liter, piece, kilogram, alcohol percentage, nicotine content, engine displacement, or other business indicators. Before implementing excise duty, clarify the tax basis first.

Common design questions:

| Question | Example |

|---|---|

| Tax basis | Amount, quantity, volume, weight, or concentration |

| Rate tiers | Different rates for low and high concentration |

| VAT interaction | Whether excise duty is included in the VAT tax base |

| Product fields | Whether volume, concentration, or grade must be stored |

| Reporting basis | Whether excise duty amount must be reported separately |

For a clear example, consider Italy's e-liquid duty based on nicotine content.

Key rate example:

- E-liquid at or below 15 mg/ml, including nicotine-free products: EUR 0.15 per ml.

- E-liquid above 15 mg/ml: EUR 0.20 per ml.

Calculation:

- Duty is calculated by bottle volume: duty = rate per ml x bottle volume in ml.

- The rate is determined by whether the bottle exceeds 15 mg/ml nicotine.

- For retail price calculation, the duty is often added to the price base first, then VAT is applied according to local rules. The examples below use 22% VAT only for demonstration.

Always verify official announcements or a tax advisor, because rules differ by product and can change over time.

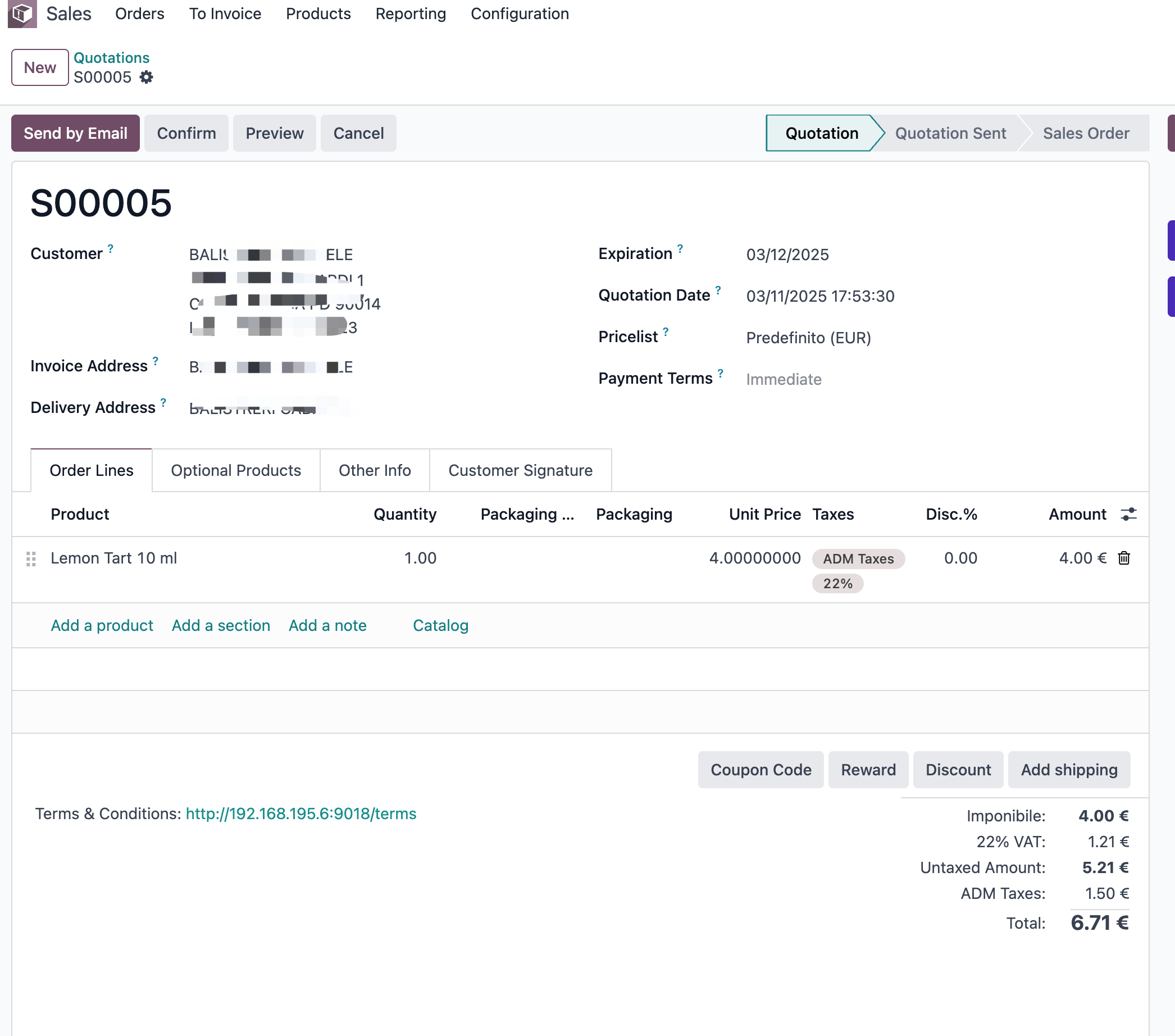

Example 1: 10 ml Bottle, Low Concentration

Configuration: 10 ml, 6 mg/ml.

Rate: EUR 0.15 per ml.

Calculation:

- Excise duty = EUR 0.15 x 10 = EUR 1.50 per bottle.

- If net factory price is EUR 4.00:

- Price before VAT = EUR 4.00 + EUR 1.50 = EUR 5.50.

- VAT = 22% x EUR 5.50 = EUR 1.21.

- Final price is approximately EUR 6.71 before retailer markup.

Example 2: 10 ml Bottle, High Concentration

Configuration: 10 ml, 20 mg/ml.

Rate: EUR 0.20 per ml.

Calculation:

- Excise duty = EUR 0.20 x 10 = EUR 2.00 per bottle.

- If net factory price is EUR 4.00:

- Price before VAT = EUR 4.00 + EUR 2.00 = EUR 6.00.

- VAT = 22% x EUR 6.00 = EUR 1.32.

- Final price is approximately EUR 7.32.

Implementing In Odoo

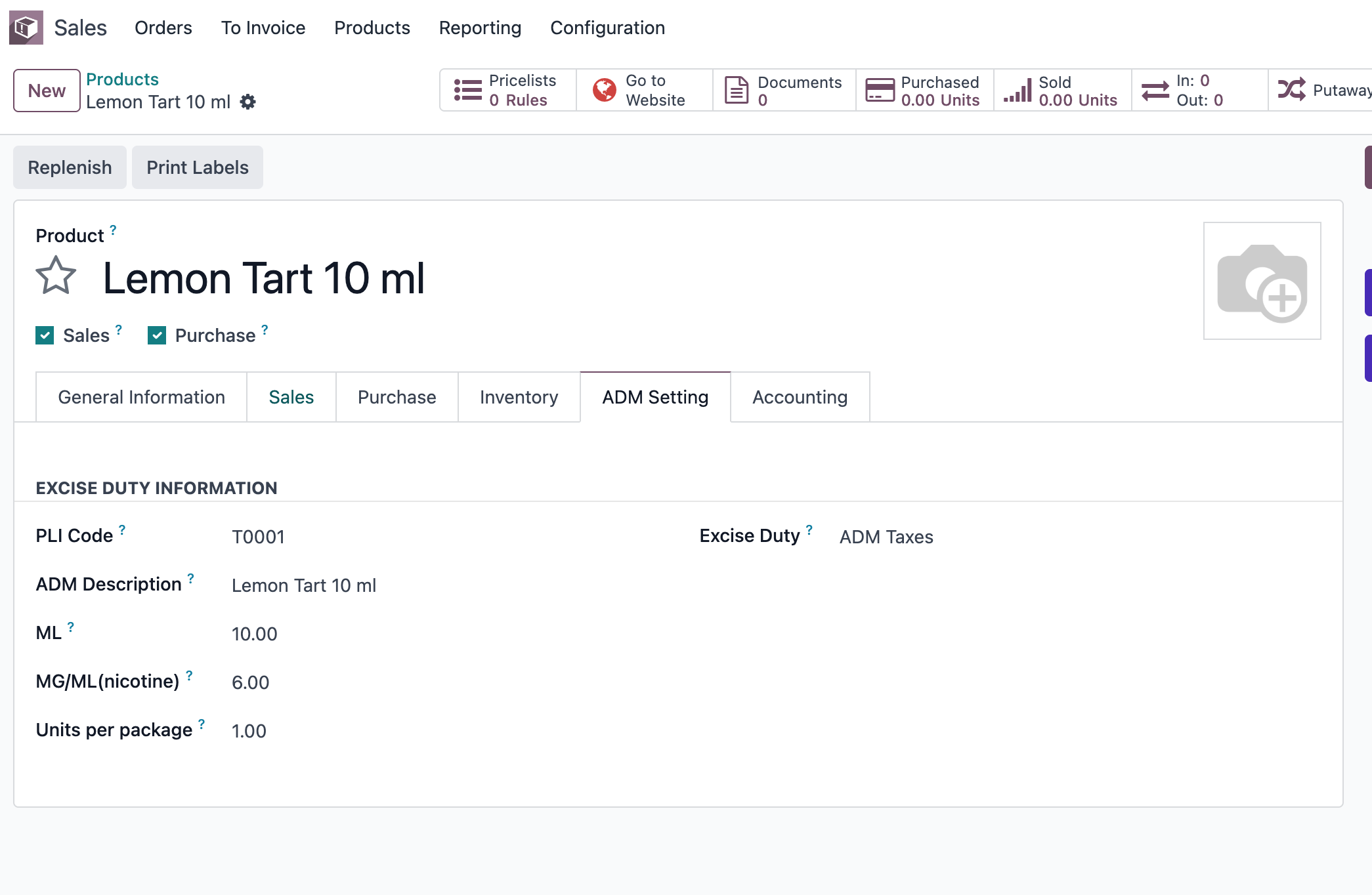

Now use a low-concentration e-liquid product, Dinner Lady, as an example to show excise duty calculation in Odoo.

Scenarios like excise duty usually cannot be solved only by a standard tax percentage. Product records often need additional attributes such as volume, concentration, whether it is a controlled consumer product, and other information that participates in tax calculation.

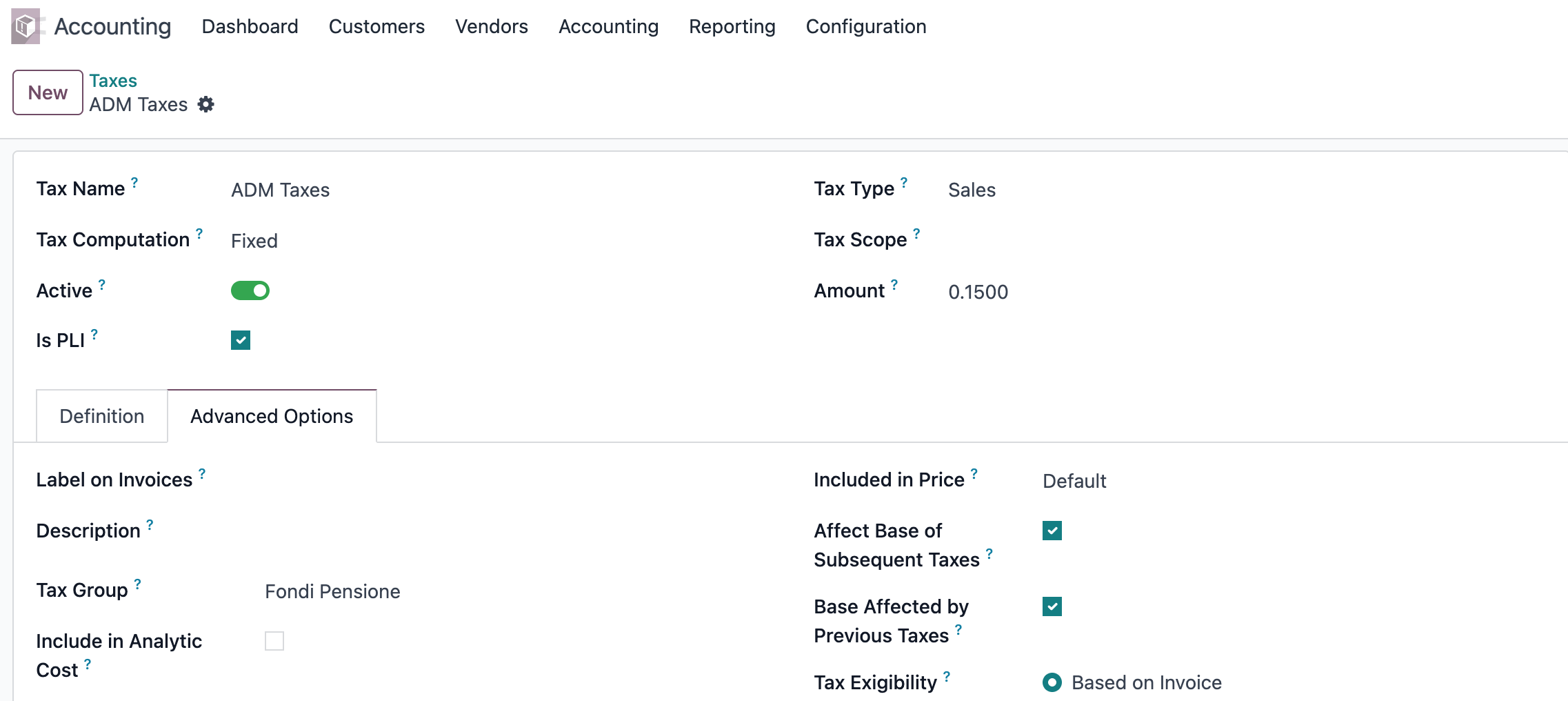

Define Excise Duty

Because the measurement basis differs from ordinary percentage taxes, the tax must be identified as excise-related on top of standard tax configuration.

In this example, the "Is PLI" option identifies e-liquid products.

Create The Product

Next, create a product named Lemon Tart 10 ml.

This product has nicotine concentration of 6 mg/ml, e-liquid volume of 10 ml, and sales price of EUR 4.

Excise Duty Calculation

Create a sales order and calculate the excise duty using Italy's common 22% VAT rate.

The result in Odoo matches the theoretical calculation. The key point is that the taxable quantity for excise duty is the e-liquid content, not simply the sales order quantity.

For this kind of tax, do not let salespeople manually change tax amounts. A more stable approach is to let product data, tax configuration, and calculation logic determine the tax amount together. Sales users should only choose the correct product and quantity.

If the customer's industry involves alcohol, tobacco, fuel, e-cigarettes, luxury goods, or other special taxes, ask finance or a tax advisor to confirm rules before sales go-live. Then decide whether the solution should use native taxes, fiscal positions, or custom tax calculation.

This chapter explained how an industry-specific tax such as excise duty extends standard sales tax logic. The next chapter covers secondary units, solving the need to express auxiliary quantities in sales, purchase, and inventory.