Chapter 12 Inventory Cost Valuation

Odoo supports several costing and inventory valuation methods. The most common methods are Standard Price, Average Cost, and FIFO. This chapter explains where to configure costing methods and how the methods differ in real inventory operations.

Costing is not only a finance topic. Product cost affects inventory value, sales margin, manufacturing cost, and management reports. Before go-live, finance, warehouse, and purchasing should agree on the cost method by product category.

Configure Costing Method

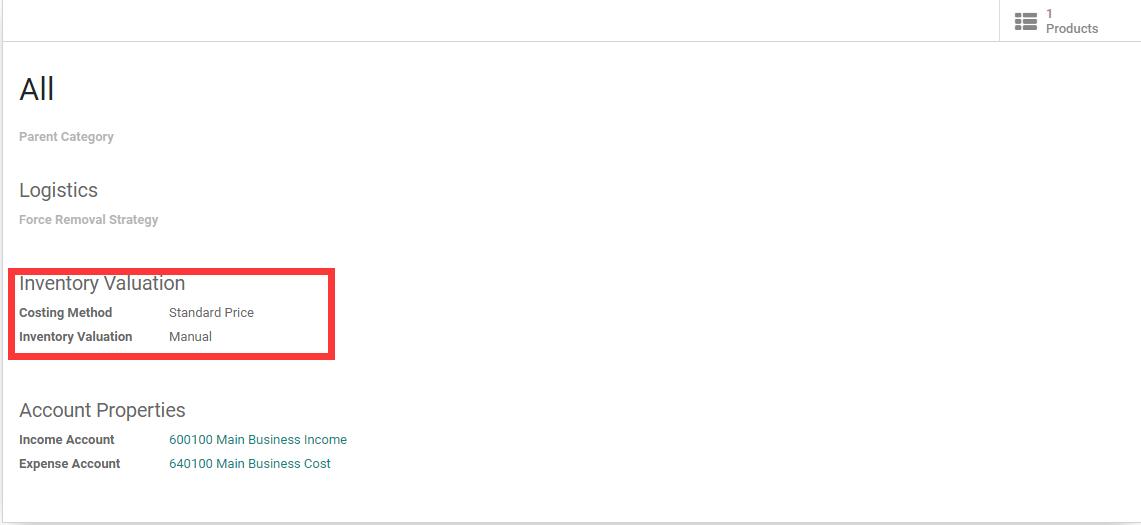

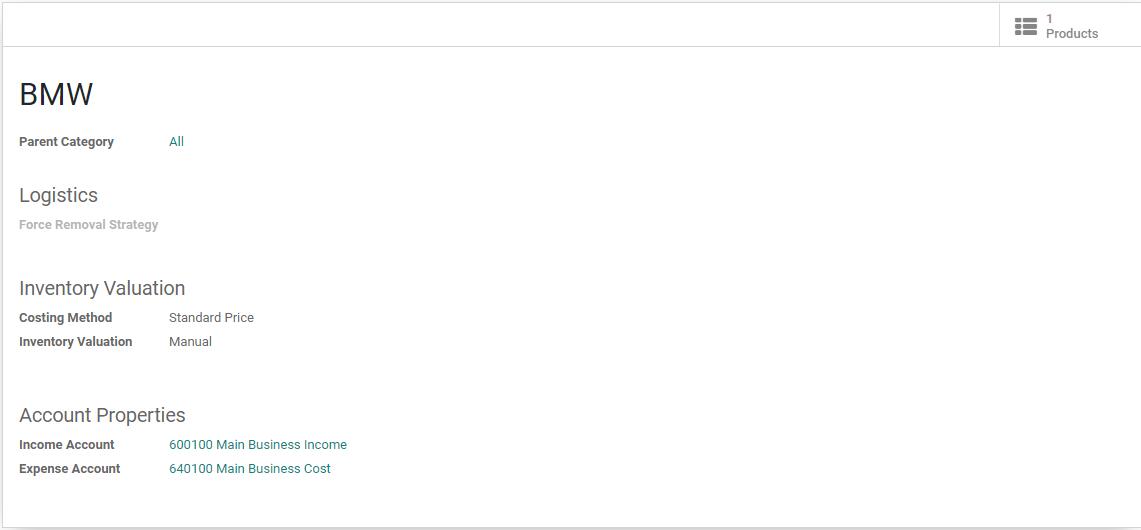

In Odoo 12 and earlier, costing method could be set directly on the product, and the system would fall back to the product category when the product did not define it. Since Odoo 13, Odoo moved this configuration to the product category. Product forms mainly reference the category setting.

Costing method is configured on the product category.

Common costing methods include:

| Method | Meaning |

|---|---|

| Standard Price | Use the cost defined on the product |

| Average Cost | Use weighted average cost |

| FIFO | Use first-in-first-out valuation |

Inventory valuation can be:

| Valuation | Meaning |

|---|---|

| Manual | Accounting impact is handled manually |

| Automated | Accounting entries are generated when stock moves happen |

The next sections explain the three cost methods.

Standard Price

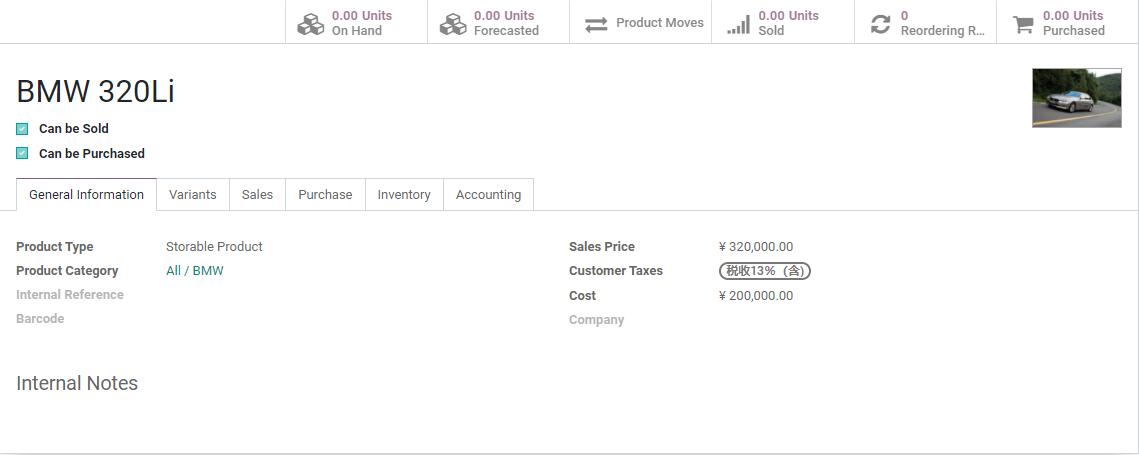

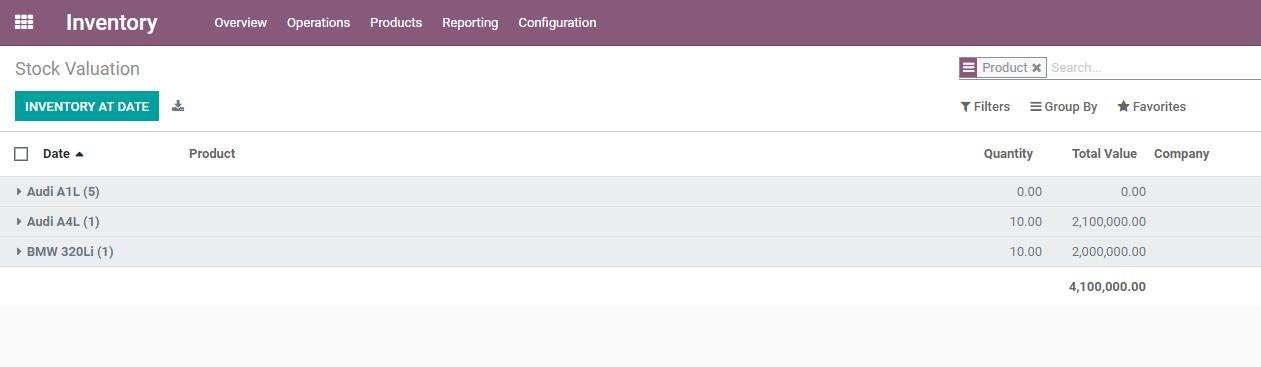

Create a BMW 320Li product and set its cost to 200,000. Set the BMW product category to Standard Price.

Then create a purchase order for 10 units at 250,000 each and receive them into stock. Because the product uses Standard Price, the cost of 320Li does not change after purchase. It remains 200,000 per unit.

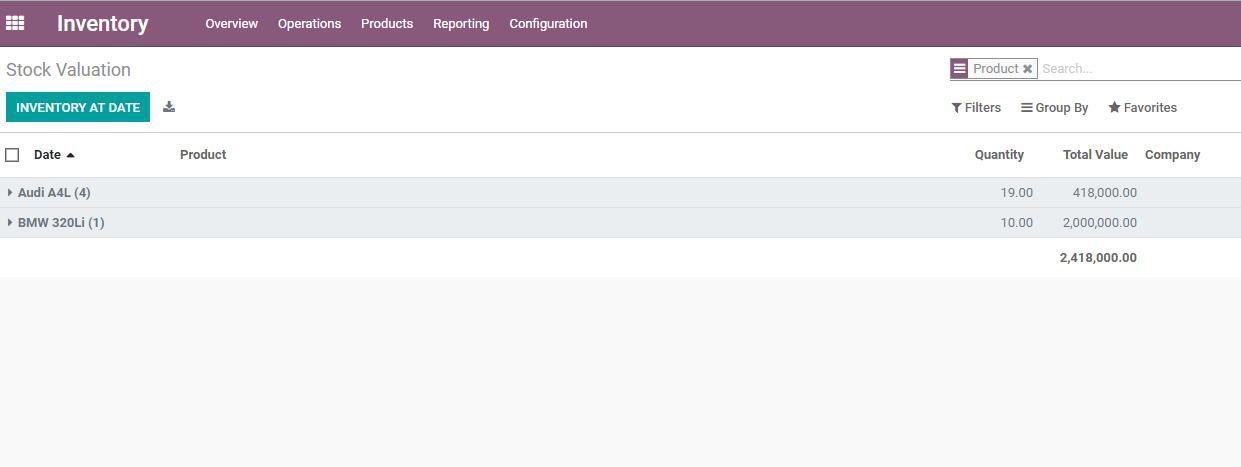

When checking inventory valuation, 10 units are valued at 2,000,000.

This shows that Standard Price does not use purchase price changes to update inventory valuation. It uses the standard product cost.

Standard Price is suitable when the company wants a controlled cost basis, or when purchase price changes should not automatically change product cost.

Average Cost

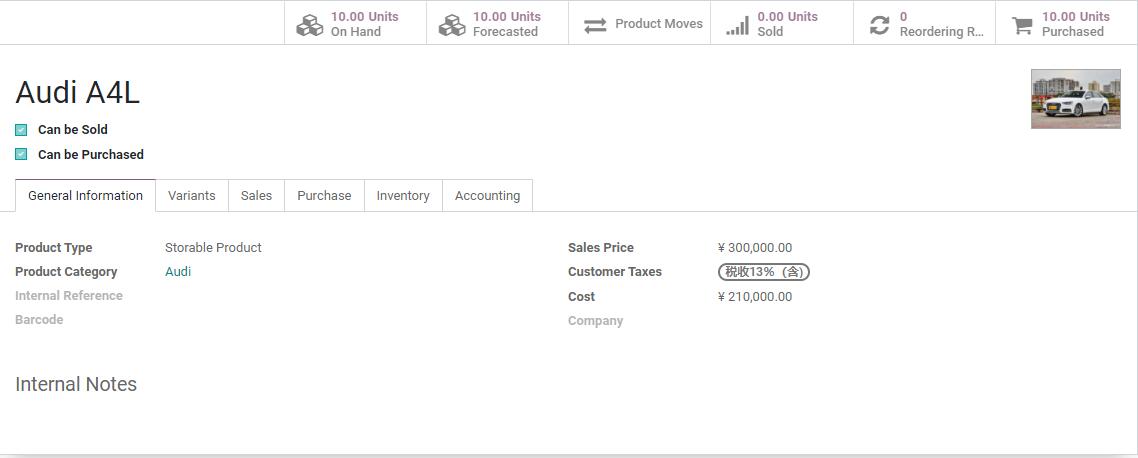

Now look at Average Cost. Use Audi A4L as an example. Set the initial cost to 0, then purchase 10 units at 210,000 each. After receipt, the cost becomes 210,000.

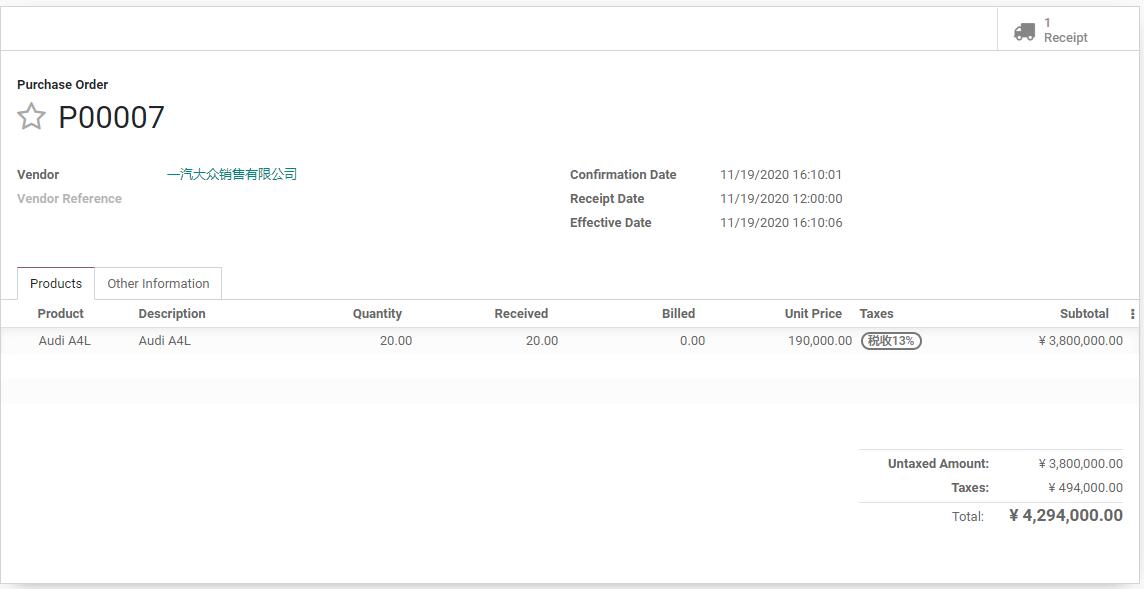

Then create a second purchase. Suppose the vendor has a promotion and each car is 20,000 cheaper. Purchase 20 units at 190,000 each.

The average cost should be:

(Existing stock value 2,100,000 + Incoming value 3,800,000) / (Existing quantity 10 + Incoming quantity 20)

= 196,666.67

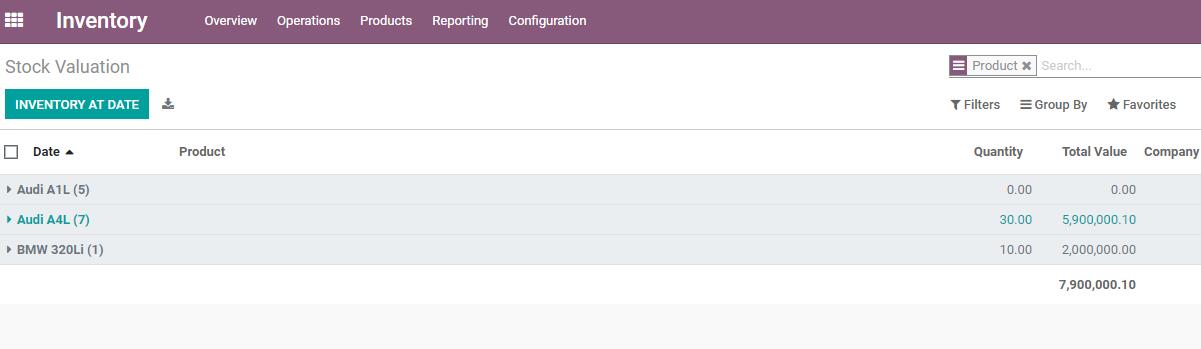

Current inventory valuation:

Average Cost changes after each receipt. The general formula is:

New average cost = (Current stock value + Incoming stock value) / (Current quantity + Incoming quantity)

Under Average Cost, selling one unit reduces inventory value by the same average cost. Sales delivery does not change the average cost itself.

Internal Logic Of Average Cost

In Odoo 12, stock.move had fields such as remaining_qty and remaining_value to store remaining quantity and value. From Odoo 13 onward, these fields were removed and Odoo introduced stock.valuation.layer.

Stock valuation layers record the value impact of receipts, deliveries, and adjustments. They are important for tracing inventory value and explaining cost changes.

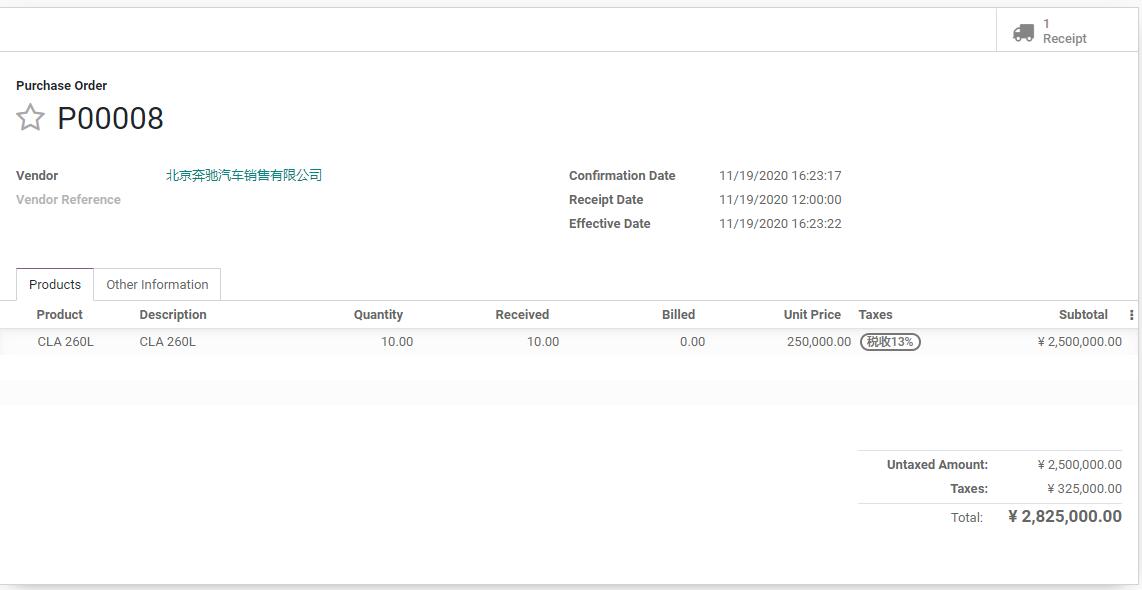

FIFO

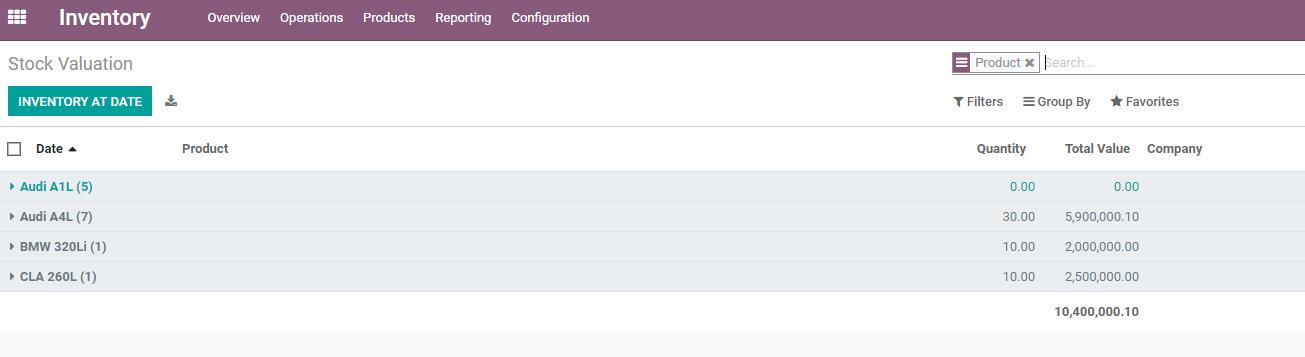

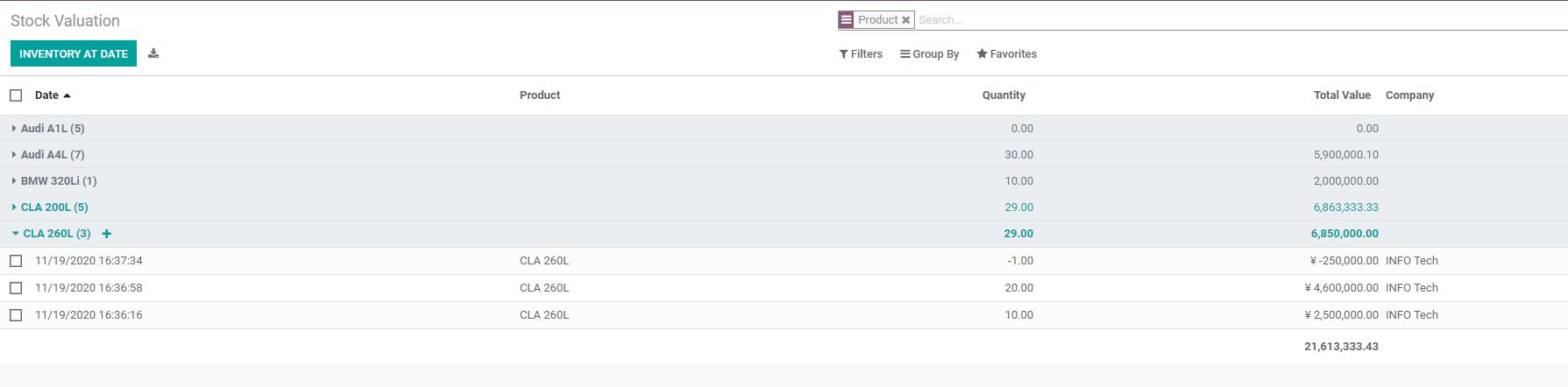

Finally, look at FIFO costing. Use Mercedes CLA 260L as an example. Do not set a starting cost. Purchase 10 units at 250,000 each. Inventory value becomes 2,500,000.

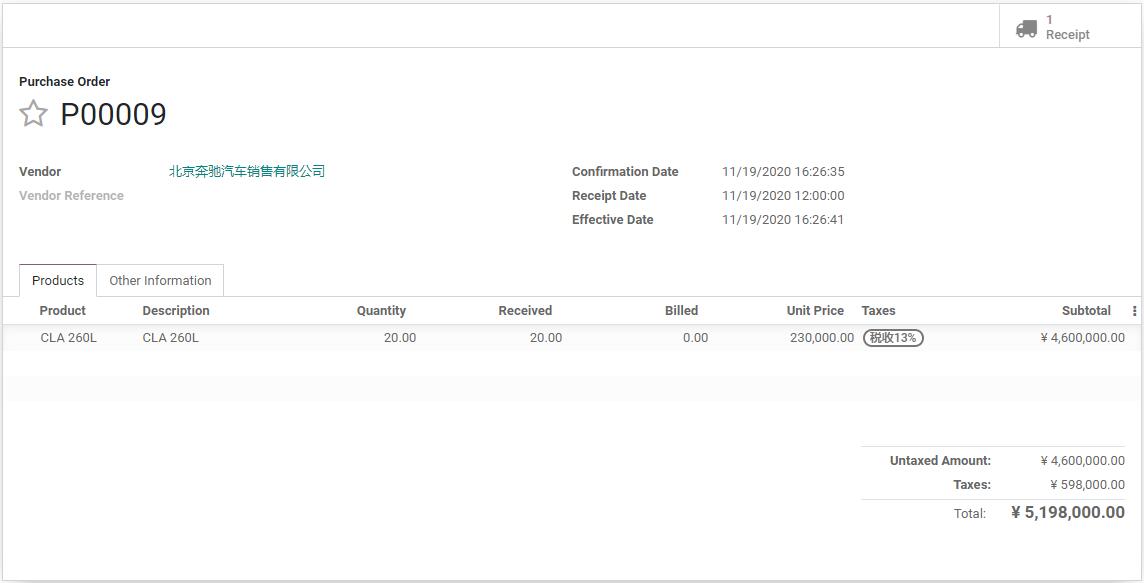

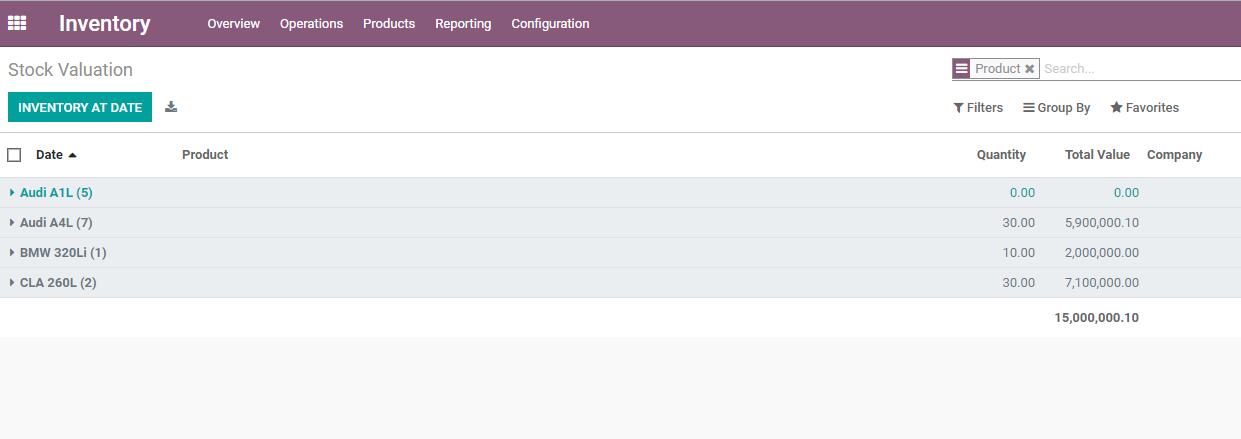

Then purchase 20 units at 230,000 each. According to FIFO, the stock valuation after receipt should be:

2,500,000 + 4,600,000 = 7,100,000

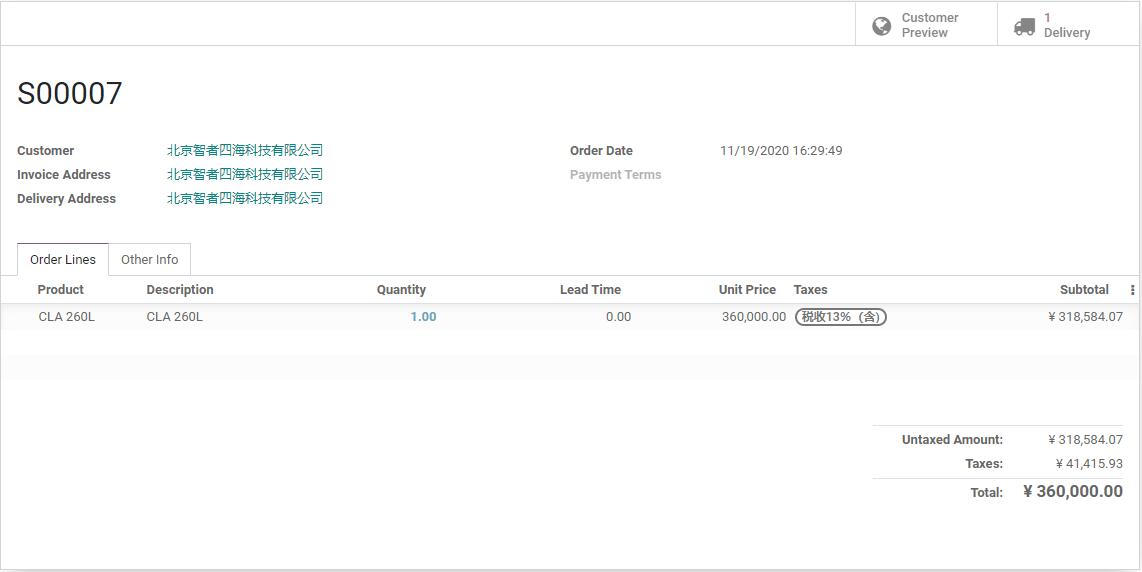

Then sell one CLA 260 at 360,000.

According to FIFO, the outgoing unit is taken from the earliest incoming layer, whose cost is 250,000. After the sale, inventory value should be:

7,100,000 - 250,000 = 6,850,000

Under FIFO, receipts and deliveries do not simply overwrite the product cost. Inventory value is calculated according to the sequence of valuation layers.

Implementation Advice

Costing method should be decided before real transactions begin.

| Scenario | Common Choice |

|---|---|

| Stable standard cost control | Standard Price |

| Purchase prices fluctuate and average cost is acceptable | Average Cost |

| Need first-in-first-out valuation or batch-like cost flow | FIFO |

| Strict accounting integration | Automated valuation, after finance review |

Do not change cost methods casually after go-live. Existing stock valuation, accounting entries, and sales margin reports may be affected.

This chapter explained Standard Price, Average Cost, FIFO, and inventory valuation layers. With this, the warehouse management part has covered the core inventory flow from locations and transfers to replenishment, barcode operations, putaway, storage categories, delivery methods, and cost valuation. The next part moves into Manufacturing, where inventory is consumed and transformed into finished goods.